How Cryptography in Blockchain Prevents Transaction Fraud

Learn how cryptography in blockchain prevents transaction fraud with secure chain block, digital signatures, and blockchain architecture.

Fraud has become one of the biggest threats to modern businesses.

With so many transactions happening digitally every day, it’s natural to wonder if your money is really safe. Many people and businesses share the same fear, what if a hacker finds a way to tamper with the payment or steal sensitive details?

A PwC survey shows that nearly 47% of companies worldwide faced fraud in the past two years.

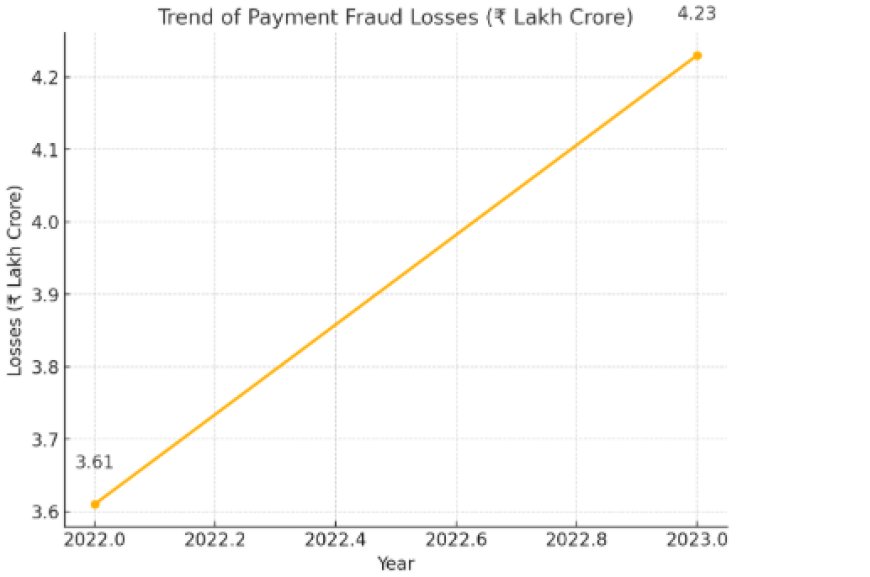

Payment fraud alone caused about ₹3.61 lakh crore in losses in 2022, and experts predict it could rise to about ₹4.23 lakh crore in 2023. Adding to this, IBM Security reports that the average cost of a single data breach is now about ₹39.2 crore, putting heavy pressure on companies to adopt stronger safeguards.

Walmart, one of the world’s largest retailers, manages a massive supply chain involving farmers, suppliers, distributors, and retail stores. With such a wide network, maintaining accuracy and transparency in records was becoming increasingly difficult.

The traditional supply chain process depends on manual records and disconnected systems. This created delays in tracking, made it easy for errors to occur, and left space for fraud or tampering.

To overcome these problems, Walmart partnered with IBM to create the IBM Food Trust blockchain system, which uses cryptography in blockchain. Every transaction, from the farm to the retail shelf, was recorded on a blockchain. Cryptography ensured that once data was entered, it could not be changed without detection. Digital signatures verified the authenticity of each entry, and transparency was built into the system.

Understanding Cryptography in Blockchain

Cryptography in Blockchain refers to the use of encryption techniques to secure data, validate identities, and protect transactions within the blockchain network. It ensures that every piece of information stored or exchanged cannot be altered, hacked, or accessed by unauthorized users.

In simple terms:

-

Hashing makes transaction records tamper-proof.

-

Public and private keys enable secure communication between users.

-

Digital signatures verify authenticity and prevent fraud.

Why Cryptography Matters in Blockchain Security

Blockchain is often described as “unhackable,” but what truly gives it this strength is cryptography in blockchain. Without cryptographic techniques, blockchain would simply be a digital ledger vulnerable to the same fraud, tampering, and cyber attacks that traditional systems face.

-

Protects Data from Unauthorized Access

Cryptography ensures that only individuals with the correct private keys can access or modify transaction details. This eliminates risks of identity theft or unauthorized manipulation.

-

Guarantees Transaction Integrity

Every transaction in blockchain is encrypted and converted into a hash. Even the smallest change in data alters the hash, making fraudulent edits immediately visible. This immutability is critical for preventing fraud.

-

Builds Trust in a Decentralized Network

Since blockchain operates without a central authority, cryptography acts as the trust mechanism. It ensures that all participants in the network can validate transactions independently.

-

Prevents Double-Spending and Fraud

Through digital signatures and consensus mechanisms, cryptography blocks attempts to duplicate or falsify transactions, one of the most common anti-fraud tactics in digital systems.

-

Ensures Transparency Without Compromising Privacy

Cryptography allows transaction data to be visible and verifiable on a public ledger while keeping sensitive details encrypted, giving businesses both transparency and confidentiality.

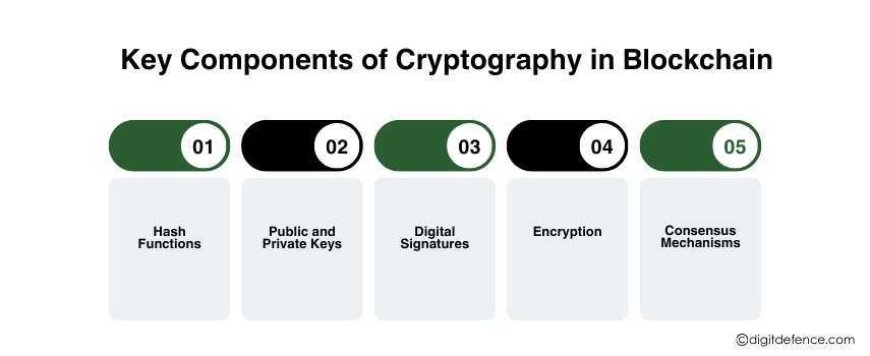

Key Components of Cryptography in Blockchain

Cryptography in blockchain is built on several critical elements that work together to secure transactions, ensure trust, and block fraudulent activity.

-

Hash Functions

Hashing turns every transaction into a unique digital fingerprint. Even a tiny change in the input creates a completely different hash, which makes tampering obvious and prevents manipulation of stored records.

-

Public and Private Keys

Every user on the blockchain has a key pair. The private key allows them to sign transactions securely, while the public key lets others verify it. This ensures only the rightful owner can authorize a transaction, protecting against fraud.

-

Digital Signatures

Digital signatures prove that a transaction really comes from the sender and hasn’t been altered. This prevents impersonation, protects authenticity, and adds accountability to every business deal recorded on the blockchain.

-

Encryption

Sensitive details within transactions can be encrypted, keeping business or customer data private while still recording the transaction on a transparent ledger. This balance of privacy and openness is a major reason businesses adopt blockchain.

-

Consensus Mechanisms

Before any transaction is added to the blockchain, it must be validated by the network. Consensus models like Proof of Work or Proof of Stake make sure no fraudulent or duplicate entries are accepted, ensuring only legitimate transactions go through.

How Cryptography in Blockchain Prevents Transaction Fraud

Fraud is one of the biggest threats in today’s digital economy, with businesses losing billions annually to payment scams, data breaches, and identity theft. Cryptography in blockchain acts as a safeguard by embedding security directly into the transaction process, making fraud extremely difficult to execute.

-

Protects Against Data Tampering

Each transaction is converted into a hash and linked to the previous block. This chain block structure means that if someone tries to alter even a small detail, the hash changes instantly, alerting the network. This immutability makes it impossible to edit records or manipulate business transactions secretly.

-

Blocks Unauthorized Access

Transactions are signed with private keys and verified with public keys. Without access to the private key, fraudsters cannot approve fake payments or impersonate legitimate users. This keeps financial records safe from unauthorized access.

-

Stops Double-Spending

One common fraud tactic in digital payments is spending the same money twice. Blockchain prevents this by validating transactions through consensus mechanisms, ensuring that once a transaction is recorded, it cannot be duplicated.

-

Verifies Authenticity with Digital Signatures

Every blockchain transaction carries a digital signature that proves it came from the actual sender. This prevents fraudsters from forging transactions or faking approvals. Businesses gain an additional layer of accountability in every exchange.

-

Ensures Transparency and Traceability

Because blockchain operates on a distributed ledger, all participants can see and verify transaction history. This visibility discourages fraudulent attempts, as every action is permanently recorded and traceable.

Benefits of Using Cryptography in Blockchain for Businesses

Adopting cryptography in blockchain is not just about security, it’s about giving businesses a competitive edge in a digital-first world. Here are the key benefits:

-

Strong Protection Against Fraud

With cryptographic techniques like hashing, digital signatures, and private keys, businesses can prevent unauthorized access, double-spending, and data tampering. This ensures every transaction is secure and trustworthy.

-

Increased Customer Trust

When customers know transactions are protected by cryptography in blockchain, they gain confidence in the business. This transparency and accountability directly improve brand reputation and loyalty.

-

Cost Savings on Fraud Management

Traditional fraud detection systems are expensive and often reactive. Blockchain’s built-in fraud prevention reduces the need for third-party verification and lowers losses caused by fraudulent activity.

-

Better Compliance with Regulations

Data protection laws like GDPR and financial regulations demand strict security standards. Cryptography in blockchain ensures records are tamper-proof, auditable, and compliant, reducing risks of legal penalties.

-

Operational Efficiency

By removing intermediaries and enabling real-time verification, businesses save time and costs on transaction approvals. The secure design of blockchain reduces delays caused by fraud investigations or disputes.

-

Scalability Across Industries

Whether in finance, retail, healthcare, or supply chain, cryptography in blockchain adapts to different business models. This makes it a versatile solution for securing sensitive data and high-value transactions.

Challenges of Implementing Cryptography in Blockchain

While cryptography in blockchain offers strong fraud prevention and security, businesses must also consider the challenges that come with implementation. These factors often determine how successful adoption will be.

-

High Energy Consumption

Consensus mechanisms like Proof of Work (PoW) require significant computing power. For businesses, this can lead to higher operational costs and raise concerns about sustainability.

-

Complex Integration with Legacy Systems

Most businesses still rely on traditional IT systems. Integrating blockchain architecture with these systems can be complicated, requiring specialized expertise and restructuring of existing workflows.

-

Scalability Issues

As the number of transactions increases, some blockchain networks struggle with speed and efficiency. Businesses dealing with large transaction volumes may face delays if scalability is not addressed.

-

Regulatory Uncertainty

Governments worldwide are still developing policies around blockchain. This lack of clear regulations can make businesses cautious about investing heavily in blockchain-based solutions.

-

Skills and Knowledge Gap

Implementing and maintaining blockchain requires specialized cryptography and blockchain expertise. Many businesses struggle to find professionals with the right skills, leading to delays and added training costs.

-

Security Risks from Poor Implementation

While blockchain itself is secure, mistakes in coding smart contracts, managing private keys, or setting up infrastructure can still lead to breaches. Businesses must follow strict practices to avoid such risks.

Today, businesses face growing risks from fraud and data breaches. Cryptography in blockchain helps solve this by making every transaction secure, transparent, and tamper-proof. The biggest benefit it brings is trust, customers, partners, and regulators know that your transactions are safe. It also reduces fraud costs, keeps businesses compliant, and builds a stronger reputation.

Protect your business from fraud with blockchain security and the right blockchain architecture. Get started today. Reach us at [email protected]